In-Depth Analysis: IREIT Global’s AGM Responses Highlight Key Challenges and Strategic Updates

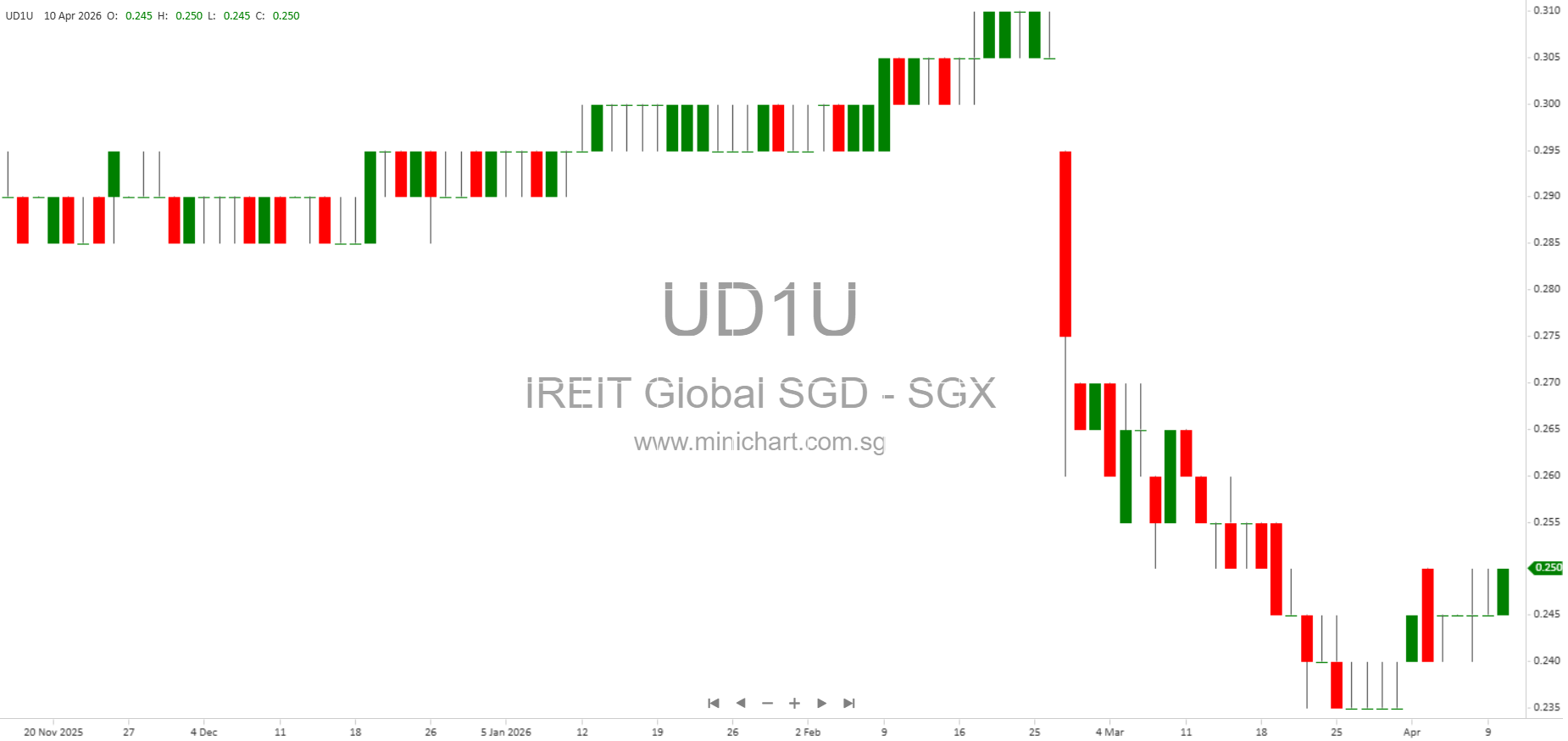

IREIT Global Group Pte. Ltd. has published its detailed responses to questions from the Securities Investors Association (Singapore) (SIAS) in advance of its Annual General Meeting (AGM) scheduled for 17 April 2026. The responses provide critical insights into the REIT’s performance, strategic direction, capital management, and board effectiveness, with several points that may be of significant interest to shareholders and could potentially impact the unit price.

1. Total Unitholder Returns – Persistent Underperformance

- 5-Year Return: -33.6% (2021-2025)

- 8-Year Return: -31.3% (2018-2025)

- Since Listing (Aug 2014-2025): -21.4%

These figures are calculated with distributions reinvested and adjusted for all rights and preferential offerings. The negative total returns over all major time periods reflect sustained underperformance, which is likely to be a material concern for current and potential investors, and could influence unit price direction.

2. Board Composition and European Real Estate Competency

A key issue raised concerns the Board’s depth of direct real estate and European market experience. The Board acknowledges that while only one independent director has substantial European asset experience, steps are being taken to address this through:

- Periodic reviews of board composition to ensure a balanced mix of skills and experience

- Continuous training and professional development, including property tours and direct engagement with European market participants

- Rigorous, collective board decision-making processes and active challenge of management proposals

While the Board highlights ongoing efforts to upskill and diversify, the current expertise gap in European real estate among independent directors may remain a point of investor concern, especially given the REIT’s strategic focus.

3. Board and Manager Performance Evaluation

The Nominating and Remuneration Committee (NRC) employs a formal annual evaluation system using performance forms that assess the effectiveness of the Board, its committees, and individual directors. Evaluation criteria include board composition, accountability, risk management, and director participation. This formalized process is intended to ensure strong governance and oversight.

4. Project RE:O / RE(O – Berlin Campus Repositioning

The Berlin Campus repositioning (Project RE:O, now named Project RE(O)) remains a cornerstone initiative:

- Phase 1 Capex: €80-90 million

- Construction Progress (as of April 2026): Premier Inn (23%), Stayery (21%)

- Expected Delivery: Q2-Q3 2027 for Phase 1; final handover to hospitality tenants (Premier Inn and Stayery) by October 2027

- Delays: Project running behind original schedule due to timeline adjustments after contractor selection

- Risk Mitigation: Fixed price/timeline contract, budget contingencies, and strict control of variation orders. Any budget deviation requires Board approval.

Any further construction delays or cost overruns could be price sensitive. The transition of major tenants out of the German Portfolio (GMG vacating Darmstadt and Münster Campuses in 2022 and DRV vacating Berlin Campus in December 2024) has shifted the portfolio from “core plus” to “value-add,” raising overall risk and potentially impacting rental cash flows.

5. Funding, Leverage, and Distribution Policy

- Current Leverage: 44.6%, which is at the high end for the REIT sector in Singapore.

-

Funding for Project RE(O):

- S\$85 million (approx. €58m) fixed rate green notes issued in May 2025 (coupon: 6.17%)

- €20 million capex facility (secured October 2025, undrawn as of 31 Dec 2025)

- €12.5 million shareholder loan from City Developments Limited (undrawn as of 31 Dec 2025)

- Equity Fund Raising (EFR): While the manager intends to avoid EFR, this cannot be ruled out for Phase 2 if capital recycling and debt headroom prove insufficient. This is a material risk to distributions and unit price.

- Distribution Policy: Manager intends to maintain regular dividend payments but warns that EFR or even a suspension of distributions could be considered if required by funding needs.

The high leverage, significant capex needs, and potential for EFR or distribution suspension are highly price sensitive matters that shareholders should closely monitor.

6. Debt and Interest Rate Risks

- Average Cost of Debt: Rose sharply from 1.9% to 2.8% (as at 31 Dec 2025)

-

Drivers:

- 6.17% coupon on green notes

- German Portfolio loan margin increased to 2.5% (from 0.73%) due to higher perceived risk after major tenant exits and portfolio transition to “value-add”

- General rise in global interest rates and credit spreads post-2019

The significant increase in debt cost reflects both changing market conditions and a material deterioration in the portfolio’s credit profile. This impacts distributable income and could weigh on unit price.

7. Management Incentives and Alignment with Unitholders

- KPIs for C-level Bonuses: Distributable income, distribution per unit, Berlin Campus project milestones, sustainability, gender diversity, and corporate culture

- Performance-Related Compensation: 40-46% of CEO/KMP pay is in long-term restricted stock units (RSUs) under Tikehau Capital’s group share plans

- Potential Misalignment: Some RSUs are linked to parent company (Tikehau Capital) performance, not directly to IREIT’s performance. The Board, however, believes this does not prejudice unitholder interests due to retention mechanisms and cost structures.

There may be investor concern regarding the degree of alignment between management interests and unitholder value, given the structure of the incentive plans.

8. Consideration of Internalisation of Management

- The Board and Independent Directors regularly review the management model, including the possibility of internalising management.

- Key prerequisites for internalisation include: larger asset base, demonstrable net benefit, proven talent acquisition, stronger alignment, regulatory feasibility, and prudent funding.

- No formal decision to internalise has been made, but the Board will update the market if and when a formal review is initiated.

A shift to internal management could have significant cost and governance implications for unitholders and may be a future catalyst.

9. Other Notable Points

- The Manager continues to benchmark fees, enhance performance-linked remuneration, and strengthen independent oversight of related party transactions.

- Any major changes, such as equity fundraising or management internalisation, would be subject to unitholder and regulatory approvals.

Conclusion: Multiple Price-Sensitive Issues for Investors

Investors should note the following key risks and potential catalysts:

- Sustained negative total returns

- Project delays and cost overruns for Berlin Campus

- High leverage and rising cost of debt

- Plausibility of equity fundraising or distribution suspension

- Potential misalignments in management incentives

- Possible future management internalisation

These factors may materially affect IREIT’s unit price, and developments should be closely watched, especially any Board updates regarding capital raising, payout policy, or management structure.

Disclaimer: This article is for informational purposes only and does not constitute investment advice or a recommendation to buy or sell securities. Past performance is not indicative of future results. The information is based on IREIT Global’s published responses as of April 2026 and may be subject to change. Please consult your financial adviser before making investment decisions.