Utah Medical Products, Inc. (UTMD) 2025 Annual Report: Detailed Investor Update

Executive Summary

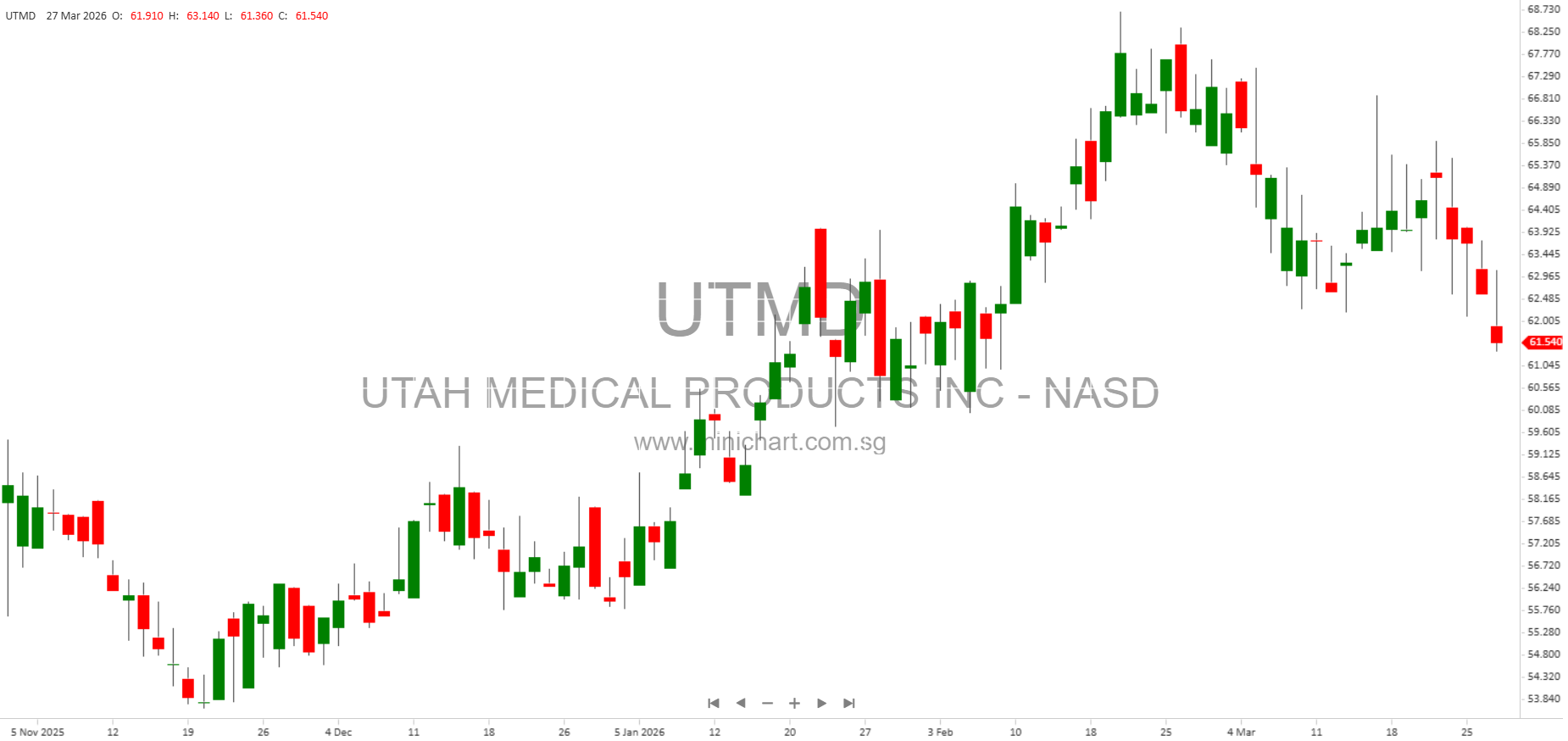

Utah Medical Products, Inc. (NASDAQ: UTMD) has released its Form 10-K for the year ended December 31, 2025. The report details a challenging year for the Company, with earnings and revenues declining compared to 2024. Nonetheless, UTMD remains in a strong financial position, maintaining robust profit margins, high liquidity, and actively returning value to shareholders via dividends and share repurchases.

Key Financial Highlights

- 2025 Revenues: \$38.52 million, down 5.8% from \$40.90 million in 2024.

- Net Income (US GAAP): \$11.29 million, a decrease of 18.7% from \$13.87 million in 2024.

- Earnings Per Share (EPS): \$3.48, down 12.1% from \$3.96 in 2024.

- Operating Income: \$11.40 million, down 16.1% from \$13.59 million in 2024.

- Gross Profit: \$22.00 million, down 8.9% from \$24.14 million in 2024.

- Year-End Cash Balance: \$85.8 million (an increase, despite dividends and buybacks).

- Current Ratio: 37.6 at end of 2025 (up from 25.6), indicating high liquidity.

- Public Float: \$168.2 million as of June 30, 2025.

- Shares Outstanding: 3,185,025 as of March 26, 2026.

Shareholder Returns

- Dividends: 2025 total cash dividends per share were \$1.22, up from \$1.20 in 2024.

- Share Repurchases: In 2025, the Company repurchased 148,935 shares for \$8.36 million (average price \$56.10/share). In 2024, 301,961 shares were repurchased for \$19.97 million (average price \$66.13/share). An additional 1,196 shares were repurchased through March 23, 2026.

Operating Results and Key Events

-

Revenue Decline Drivers:

- PendoTECH OEM Sales: Major reduction (-\$1.04 million) due to the loss of a key OEM customer. UTMD does not expect these revenues to recover.

- China Distributor Issue: UTMD’s China distributor canceled a previously non-cancellable order for blood pressure monitoring kits, resulting in \$431,000 lower revenues than committed, and \$310,000 lower sales vs. 2024. About \$400,000 of 2025 sales were written off as an uncollectible receivable.

-

Filshie Device Sales:

- US Domestic Sales: Dropped 16% to \$4.5 million.

- OUS (Outside U.S.) Distributors: Down 23% to \$1.1 million.

- Total Filshie Revenues: Decreased 7% to \$10.1 million.

-

Operating Expenses:

- Higher costs due to salary adjustments and inflation in raw materials.

- Legal costs (mainly Filshie clip litigation) decreased by \$783,000 in 2025, but this benefit was offset by:

- \$395,000 write-off from China distributor cancellation fees

- \$195,000 loss from embezzlement by the Australia subsidiary manager

- \$100,000 increase in OUS G&A expenses due to stronger EUR and GBP

- Profit Margins: Declined, with Net Income margin falling to 29.3% (from 33.9% in 2024). Income before tax margin (EBT/sales) was 36.6% (down from 41.1%).

- Foreign Exchange (FX) Impact: Significant portion of revenues invoiced in foreign currencies; currency fluctuations affected both sales and expenses.

- Cash Position: Despite share repurchases and dividends, cash balances grew, indicating strong cash generation from operations.

Business and Strategic Overview

- Product Focus: UTMD specializes in high-quality medical devices differentiated by safety and improved patient outcomes. Its strategy relies on responsiveness to clinician needs, rapid product development, and effective direct and distributor sales channels.

- Geographical Exposure: UTMD serves both the U.S. and international markets, with reliance on third-party distributors in some regions. The Company highlighted risks related to unpredictable regulatory and geopolitical environments, especially in countries like China, Pakistan, and India.

- Patent and IP: UTMD owns several unexpired U.S. and international patents, and licenses additional technology. The Company defends its IP vigorously but notes risks from competitors and potential litigation.

- Cybersecurity: UTMD employs state-of-the-art cybersecurity protocols and has not suffered any material breaches in over three decades. The Board’s Governance Committee oversees cybersecurity risk.

Risks and Potential Share Price Movers

- Loss of OEM Revenue: The loss of a key PendoTECH OEM customer causing a \$1 million+ revenue decline may have a negative impact on future profit growth and is price-sensitive.

- China Distributor Default: The write-off of nearly half a million dollars due to the China distributor’s default highlights credit and geographic risks that could further impact revenue and profit.

- Litigation Developments: While Filshie clip litigation expenses declined in 2025, any new trials or unfavorable outcomes could drive up costs and impact future results.

- Currency Fluctuations: Ongoing FX volatility can materially impact revenues and expenses, especially given the Company’s international exposure.

- Strong Financial Position: Despite challenges, UTMD’s strong cash position and liquidity provide the flexibility to pursue acquisitions, continue buybacks, or withstand adverse conditions.

- Shareholder Returns: The Company’s continued dividend increases and share repurchases support the stock and may appeal to value-focused investors.

- Embezzlement Incident: The \$195,000 embezzlement loss in Australia is a governance red flag, though not material in size, it signals the importance of internal controls.

Other Noteworthy Items

- Market Data: As of March 2026, UTMD has about 2,000 beneficial shareholders.

- Company Structure: UTMD remains a non-accelerated filer and a smaller reporting company, not a shell company.

- No Material Cybersecurity Incidents: No significant cybersecurity events have occurred in the past 33 years.

- Acquisitions & Partnerships: UTMD continues to explore internal development, licensing, and acquisitions for growth.

Conclusion

Bottom Line for Investors: Despite a challenging 2025 marked by revenue declines and several one-off negative events, Utah Medical Products, Inc. remains highly profitable, cash-rich, and committed to returning value to shareholders. However, key risks include lost OEM contracts, distributor defaults, ongoing litigation, and FX volatility. Investors should monitor management’s ability to replace lost revenues, defend margins, and manage international risks. The Company’s strong balance sheet positions it well for future opportunities and challenges.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. Please refer to the official filings and consult your financial advisor before making investment decisions. The author and publisher assume no responsibility for investment decisions made based on this information.