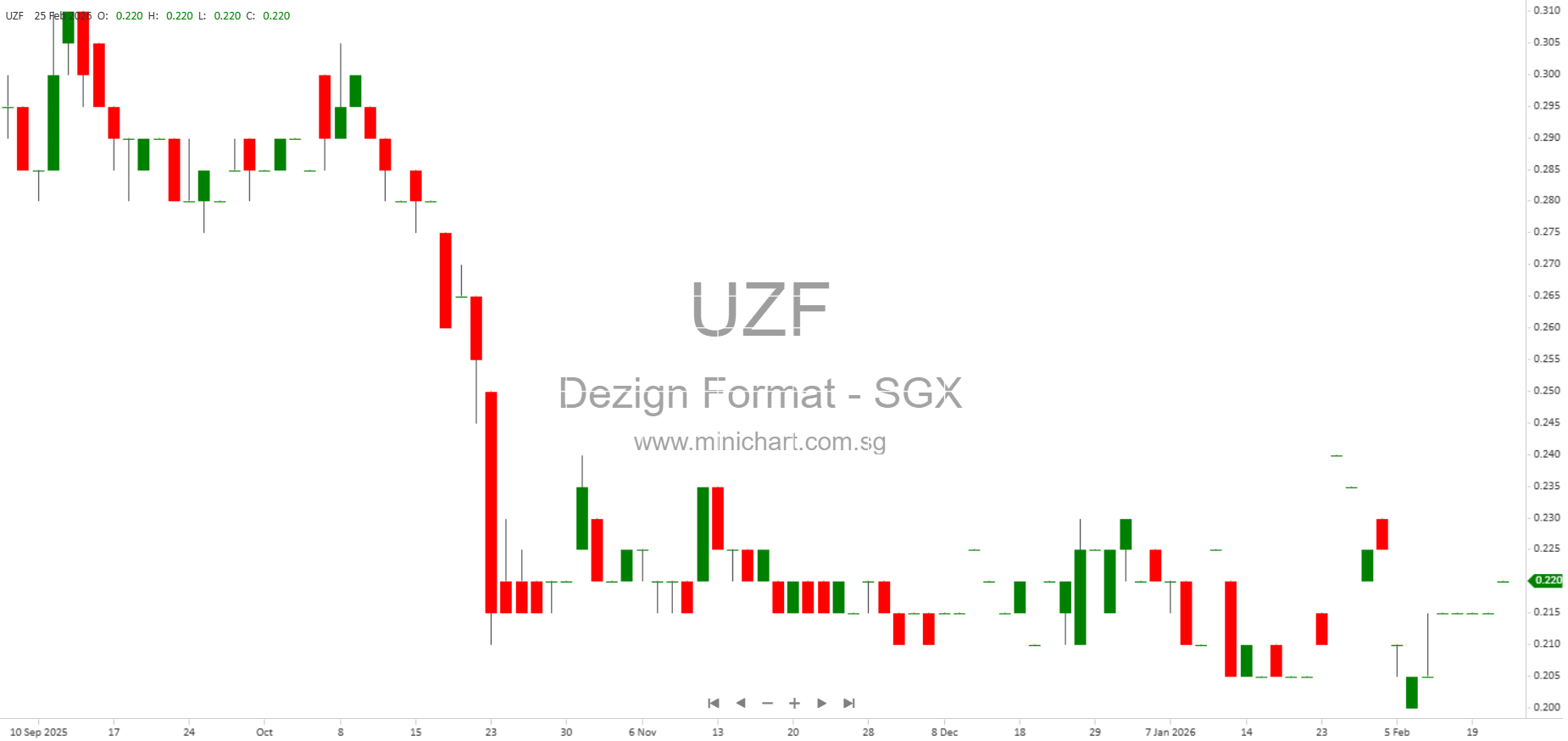

Dezign Format Group Limited FY2025 Financial Review: Navigating Challenges and Investing in Growth

Dezign Format Group Limited, recently listed on Singapore’s Catalist board, has published its condensed interim financial statements for the six months and full year ended 31 December 2025. The Group, specializing in design, fabrication, fit-out services, and immersive location-based entertainment (LBE), reported a challenging year marked by margin compression, increased costs, and ongoing investment in new business segments. Below is an in-depth analysis of key performance metrics, trends, and management commentary to help investors make informed decisions.

Key Financial Metrics and Performance Comparison

| Metric | 2H2025 | 1H2025 | 2H2024 | FY2025 | FY2024 | YoY Change | QoQ Change |

|---|---|---|---|---|---|---|---|

| Revenue (S\$’000) | 16,361 | 16,743 | 17,605 | 33,104 | 33,422 | -1.0% | -2.3% |

| Net (Loss)/Profit (S\$’000) | (306) | 1,457 | 2,781 | 1,151 | 5,028 | -77.1% | n.m. |

| EPS (cents, Basic & Diluted) | (0.15) | 0.73 | 1.66 | 0.58 | 3.00 | -80.7% | n.m. |

| Dividend (per share, cents) | 0.25 (proposed final) | — | — | 0.25 (proposed final) | — | n.a. | n.a. |

| Net Asset Value per Share (cents) | — | 5.54 | 7.06 | -21.5% | — | ||

Historical Trends and Performance Highlights

- Revenue: Relatively flat YoY, with a marginal decline of 1.0% to S\$33.1 million. Number of projects fell from 607 in FY2024 to 552 in FY2025, but average project value increased.

- Profitability: Net profit dropped sharply by 77.1% YoY, mainly due to cost pressures and increased investments in headcount, new facilities, and the LBE segment. The second half saw a net loss as compared to a profit in 2H2024.

- Margins: Gross profit margin declined from 38.8% to 35.5% YoY, affected by higher labor costs, foreign worker levies, dormitory costs, and front-loaded setup costs for the Malaysia facility.

- Expenses: General and administrative expenses surged 27.2% YoY, with one-off IPO expenses and higher legal, professional, and staff costs.

- Balance Sheet: Net asset value per share declined 21.5% to 5.54 cents, reflecting weaker profitability and a S\$5.19 million drop in the value of quoted investments (FVOCI).

- Cash Flow: Net cash outflow of S\$2.78 million, driven by working capital investment, capex for facility expansion, and dividend payments, partially offset by IPO and bank loan proceeds.

Dividends

- FY2025 Final Dividend Proposed: 0.25 cents per share, tax-exempt (one-tier), subject to shareholder approval at the AGM. No dividend was declared in FY2024 as the Company was not yet listed.

Exceptional Items & Corporate Actions

- IPO and Restructuring: The Company undertook a restructuring and IPO, raising S\$4.8 million net proceeds (after S\$1.7 million expenses). Funds are being deployed into LBE expansion, joint ventures, and working capital.

- Asset Revaluation: Significant fair value loss of S\$5.19 million on quoted financial assets at FVOCI, primarily due to share price declines.

- Malaysia Facility Investment: S\$3.53 million capex for land, building, and machinery to expand production capabilities and supply chain integration.

- Related Party Transactions: S\$395,000 in sub-contracting to Skyy Design Workshops Pte. Ltd. under a shareholder mandate, and other minor IPTs.

Chairman’s Statement

“The Group remains cautiously optimistic about its outlook for the upcoming financial year, while recognising the continued uncertainties within the global economic environment. Ongoing geopolitical tensions and inflationary cost pressures may influence business sentiment and project timelines, contributing to a more complex operating landscape for the industry.

Notwithstanding these external challenges, the Group will continue to strengthen its cost competitiveness and operational resilience. The Group intends to actively leverage its manufacturing facilities in Malaysia, alongside access to a broader ecosystem of labour, materials and subcontractor resources, to enhance supply chain integration and optimise production efficiency. These initiatives are expected to strengthen project execution capabilities, improve the cost-to-sales ratio and reinforce the Group’s ability to capture greater market share within its core design-and-build business.

In parallel, the Group remains committed to expanding its immersive Location-based Entertainment and Experiences (“LBE”) segment, which represents a key strategic growth pillar. Through continued investment in capabilities, proprietary content and project pipeline development, the Group aims to further diversify its business portfolio and capitalise on the growing demand for experiential and themed environments across the region.

Barring unforeseen circumstances, the Group is confident that these strategic priorities will further strengthen its competitive positioning, enhance operational scalability and support sustainable long-term growth over the next 12 months and beyond.”

Tone: The statement is cautiously optimistic, but acknowledges significant industry challenges and a need for cost discipline and growth execution.

Outlook and Risks

- Opportunities: Expansion in Malaysia and immersive LBE segment positions the Group for future growth and operational scale.

- Risks: Margin pressure from labor and input costs, volatility in investment portfolios, macroeconomic uncertainty, and execution risk in new ventures.

- Cash Utilization: About 55% of IPO proceeds remain unutilized, offering flexibility for further investment or buffer against headwinds.

Conclusion and Investment Recommendations

Overall Assessment: Dezign Format Group’s FY2025 performance was weak, with significant declines in profit and margins despite stable revenues. The Group faces cost pressures and is investing heavily in new segments and capacity, which may take time to yield results. The proposed dividend is modest, reflecting a cautious capital return policy post-IPO.

- If you are currently holding the stock: Consider maintaining a cautious hold. While near-term profit pressure and margin risk persist, management is actively investing for future growth and improving operational resilience. However, closely monitor quarterly performance, cash flow, and execution of growth initiatives, especially in the LBE segment. If cash burn accelerates or losses persist, reassess your position.

- If you are not currently holding the stock: Adopt a wait-and-see approach. The company’s transformation and growth plans are promising but unproven, and the business faces ongoing margin and execution risks. Await evidence of margin recovery, positive cash flow from new investments, or improved profitability before initiating a position. Near-term upside may be limited given current results and sector headwinds.

Disclaimer: This commentary is based solely on the company’s published financial report and does not constitute investment advice. Investors should conduct their own due diligence and consider their risk appetite before making any investment decisions.