Plato Capital Limited: FY2025 Financial Review and Outlook

Plato Capital Limited, an investment holding company listed on Singapore’s Catalist Board, released its condensed interim financial statements for the six months and twelve months ended 31 December 2025. Below, we analyze key metrics, performance trends, exceptional items, and the outlook for investors based strictly on the disclosed report.

Key Financial Metrics

| Metric | 2H2025 | 1H2025 | 2H2024 | FY2025 | FY2024 | YoY Change | QoQ Change |

|---|---|---|---|---|---|---|---|

| Revenue | \$330k | \$287k | \$284k | \$617k | \$544k | +13.4% | +16.2% |

| Net Profit/(Loss) | \$(4.3)m | \$611k | \$728k | \$(3.7)m | \$598k | NM | NM |

| EPS (basic, cents) | (20.82) | 5.81 | 6.34 | (15.01) | 5.42 | NM | NM |

| Dividend | None | None | None | None | None | N/A | N/A |

| Net Asset Value/share (\$) | 4.84 | 4.85 | 4.85 | 4.84 | 4.85 | -0.2% | -0.2% |

Historical Performance and Trends

- Revenue: Grew modestly year-over-year, primarily from increased credit facilities provided by Plato Capital Sdn Bhd.

- Net Loss: The Group swung from a profit in FY2024 to a significant loss in FY2025. The main driver was a \$5.04 million impairment loss on property, plant and equipment and a \$1.04 million impairment loss on financial assets.

- EPS: Turned negative, reflecting the losses.

- Net Asset Value: Slight decrease, mainly due to the impairment losses.

- Dividend: No dividends were declared for FY2025, consistent with FY2024.

Exceptional Earnings and Expenses

- Impairment Losses: Management recognized a \$5.04 million impairment loss on property, plant, and equipment following a decline in market values based on an independent valuation. An additional \$1.04 million impairment loss was recognized on financial assets, reflecting credit risk and a reassessment of receivables.

- Foreign Exchange Gains: The Group recorded a net foreign exchange gain of \$1.36 million in FY2025, mainly driven by the strengthening of the Euro and Ringgit Malaysia against the reporting currency.

- Operating Expenses: Increased significantly due to land tax on the Dublin property and higher professional fees related to the proposed voluntary delisting and capital reduction.

Asset Sales and Corporate Actions

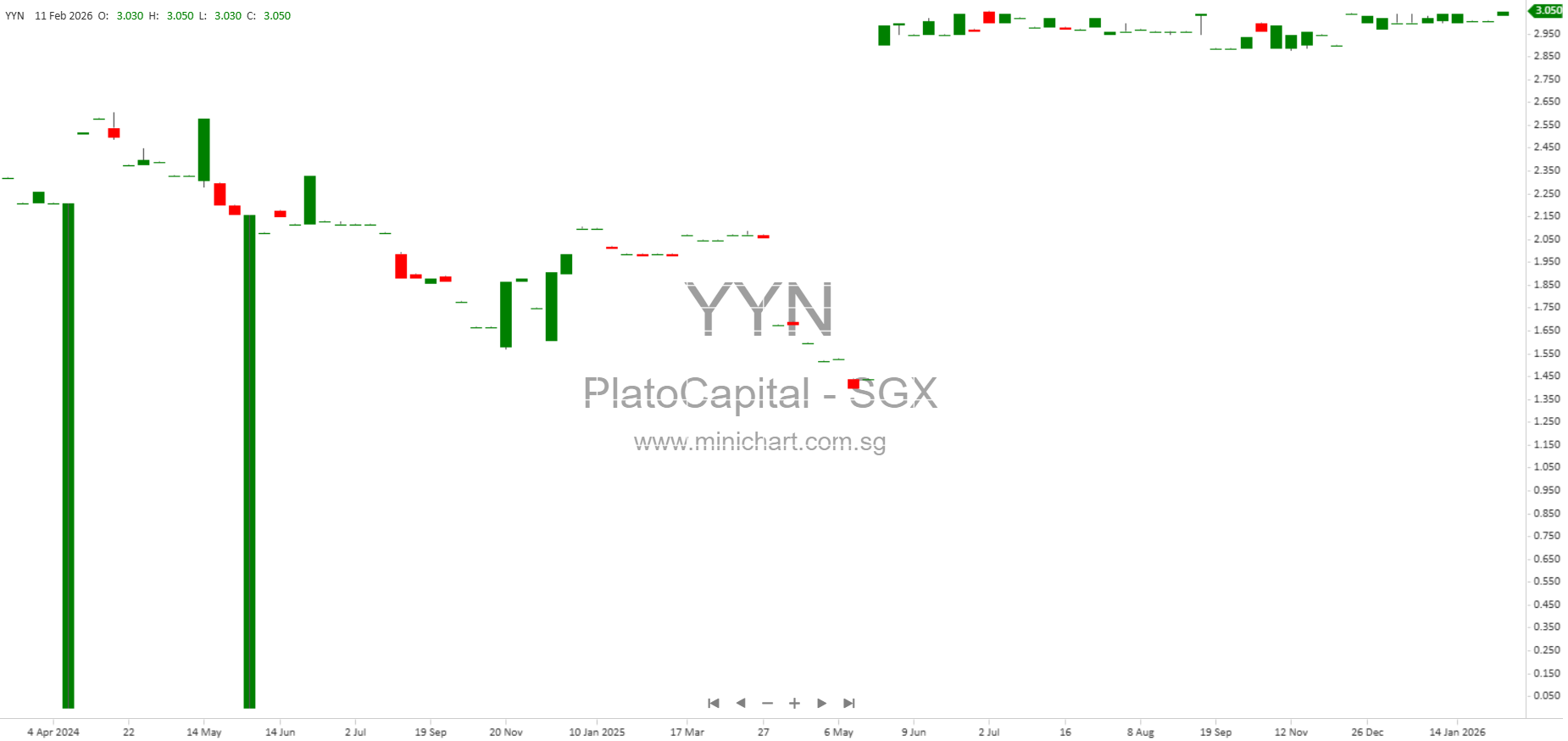

- Proposed Voluntary Delisting and Capital Reduction: Shareholders approved a selective capital reduction (\$3.05 per share cancelled) and voluntary delisting. Cash earmarked for this (\$6.38 million) is included in year-end balances.

- Disposal of Property: A joint venture (TP International Pty Ltd) entered a contract to sell a Melbourne property for AUD30 million, with a development lease agreement pending completion. This is considered part of normal business activities.

- Strike-off and Dissolution of Subsidiaries: Several dormant subsidiaries (including Plato Private Limited and Positive Carry Sdn Bhd) were struck off or dissolved, streamlining the corporate structure.

Directors’ Remuneration

| Role | 6 Months Ended 31-Dec-2025 | 12 Months Ended 31-Dec-2025 |

|---|---|---|

| Directors’ Fees | \$79k | \$158k |

| Key Management Total | \$357k | \$632k |

Related Party Transactions

- Lease Payments: Lease payments to Noblemen Holdings Sdn Bhd, a company with director interest, totaled \$55k in FY2025.

- No Major Interested Person Transactions: No transactions above \$100,000 were reported in FY2025.

Fund Flows and Liquidity

- Cash and Cash Equivalents: Decreased from \$13.86 million to \$12.63 million, mainly due to additional credit facilities granted, land tax payments, and operating expenses.

- Net Current Asset Position: Decreased to \$19.96 million from \$22.16 million, reflecting impairment losses and cash outflows for operating activities.

Outlook and Chairman’s Statement

The report does not provide a formal Chairman’s Statement but includes management commentary:

The Group remains cautiously optimistic about its outlook. The hospitality segment is expected to continue benefiting from steady regional travel flows and sustained demand in Malaysia and Japan, contributing to consistent operating performance across the Group’s hospitality assets. Management will continue to focus on enhancing operational efficiency, strengthening commercial strategies and maintaining service standards to reinforce the competitiveness of its assets. In the education segment, Epsom College in Malaysia is expected to maintain stable enrolment levels, supported by its established academic reputation and boarding proposition.

Notwithstanding ongoing macroeconomic uncertainties, including cost pressures and foreign exchange movements, management will continue to exercise prudence in cost management and capital allocation, while maintaining the flexibility to respond to changing market conditions and opportunities that support long-term value creation.

The tone is cautiously positive, with an emphasis on operational prudence and stable business segments.

Events and Corporate Actions

- Delisting and Capital Reduction: The Company is set to delist and return capital to shareholders via a selective capital reduction.

- Asset Sale: The sale of the Melbourne property is expected to impact liquidity positively.

- Subsidiary Streamlining: Strike-off and dissolution of dormant companies will reduce administrative burden.

Conclusion & Recommendations

Financial Performance: The Group’s FY2025 results were weak, driven by significant impairment losses which wiped out profits and turned earnings negative. However, core business segments (hospitality, education) remain operationally stable, and management has maintained a cautious and prudent tone.

Investor Recommendations

- If you are currently holding: Consider the imminent voluntary delisting and selective capital reduction (\$3.05 per share cancelled). Review your eligibility for the cash distribution and monitor the Company’s announcements for timing and process. With no dividend and delisting imminent, reassess your position and prepare for capital return.

- If you are not currently holding: Given the delisting and capital reduction, there is little opportunity for new investors to participate in the Company. The stock will be suspended and delisted soon, so entry at this stage is not recommended.

Disclaimer: This analysis is based strictly on Plato Capital Limited’s released financial report for FY2025. It does not constitute investment advice. Investors should consider their own circumstances, risk tolerance, and consult a qualified financial advisor before making investment decisions.