On the morning of Dec 5, 2023, shareholders of TeleChoice International woke to unwelcome news: the company had been placed on the Singapore Exchange (SGX) watchlist after four consecutive years of losses. If TeleChoice fails to meet certain criteria within 36 months, it faces the risk of delisting.

For newly appointed CEO Pauline Wong, who had just taken the helm in October 2023 after 24 years at the company, the moment was sobering. “Of course, there was an immediate sinking of the heart, to say the least,” Wong told The Edge Singapore. “It’s okay to feel lousy for a day or two — but after that, we had to snap out of it.”

Following the announcement, shareholder feedback flooded in. One investor expressed concern over the ongoing losses, while another questioned whether dividends would resume now that the company was on the SGX watchlist.

Pandemic Fallout and ‘Ground Zero’

The company’s losses stemmed primarily from the Covid-19 pandemic, which disrupted operations in Singapore and across the region. In FY2020, TeleChoice posted a net loss of $5.6 million, with revenue falling 31.9% y-o-y to $213.5 million, translating to a loss per share of 1.23 cents, a reversal from an EPS of 1.19 cents in FY2019.

FY2023 was even more difficult, with net losses widening to $11.5 million, which Wong described as “a bloodshed year.” Yet, she saw it as a turning point. “That to me — and to us — was ground zero. That was the year that marked the end of all losses.”

A Profitable FY2024

By FY2024, TeleChoice returned to profitability with a net profit of $4.2 million, buoyed by a 59.8% revenue increase to $380.4 million, and an EPS of 0.89 cents. Growth was seen across all business divisions.

Wong now calls FY2025 “the year of execution,” focused on building a “robust and sustainable” business model and growing shareholder returns.

Business Segments and Expansion

TeleChoice operates through three segments: Personal Communications Solutions (PCS), Infocomm and Technology (ICT), and Network Engineering Services (NES).

PCS – The “Star Performer”

The PCS division, TeleChoice’s core business, distributes mobile and consumer tech devices. In FY2024, revenue soared 115.9% y-o-y to $241.4 million, with profit before tax (PBT) of $6.6 million.

In Singapore, TeleChoice is the largest distributor of Samsung devices and serves as brand representative for Honor, a Huawei spin-off. Tasks such as marketing, operator onboarding, and regulatory approval fall under TeleChoice’s purview — duties typically handled by the brand.

Combined, Samsung and Honor contributed about half of the division’s FY2024 revenue.

In Malaysia, TeleChoice secured a $500 million three-year logistics contract with U Mobile, covering procurement, inventory, warehousing, and distribution across 1,002 touchpoints, including East and West Malaysia. Both companies share a common major shareholder: Singapore Technologies Telemedia, a Temasek Holdings subsidiary.

ICT – Restructured and Recovering

The ICT segment, which had been loss-making, showed notable improvement. Losses narrowed to $1.2 million in FY2024 from $7.9 million the previous year, aided by a 12% revenue rise to $85.7 million and the disposal of its telephony services business in FY2023. The segment was reorganised into three areas: digital infrastructure, tech & apps services, and communications.

Services include storage servers, cloud infrastructure, and unified communications for corporate clients.

Wong says diversification is critical: “We can’t be everything. There’s NCS, there’s ST Engineering — we can’t compete at that level. So how do we differentiate? We have to go deep in our offerings.”

The ICT arm has recently secured wins in banking, healthcare, gaming, and hospitality, with Wong noting that the AI wave will transform the space.

NES – Eyes on Indonesia

The NES segment delivers end-to-end network solutions for telecoms and data centres, offering services from planning and cabling to project management. Key partners include Huawei, China Telecom Europe, and Nokia, all active in deploying 5G networks.

Indonesia, entered via the 2023 acquisition of NexWave Technologies, is now seen as a “stronghold” for the segment, where 3,500 employees serve telcos and data centres. FY2024 revenue rose 7.5% to $53.3 million, yielding PBT of $700,000.

Wong sees future opportunities in data centre value chains and shifting from hardware to cloud services.

Diversifying Beyond Singapore

Revenue diversification is a key focus. In FY2023, 80% of revenue came from Singapore. In FY2024, Singapore contributed 56%, while Malaysia and Indonesia accounted for 34% and 10% respectively.

Aiming to Reward Shareholders

Wong is committed to creating value for shareholders, many of whom have been invested for decades. “Some of them are elderly and rely on our dividends as pocket money. It’s humbling,” she says.

For FY2024, TeleChoice introduced a dividend policy to distribute at least 30% of net profit after tax. Wong says this reflects management’s confidence in a sustained turnaround: “If this was a flash in the pan, we wouldn’t have been bold enough to announce a dividend policy.”

Historically, the company has paid 31 cents in total dividends since listing at 29 cents in 2004, distributing 96% of total earnings to shareholders.

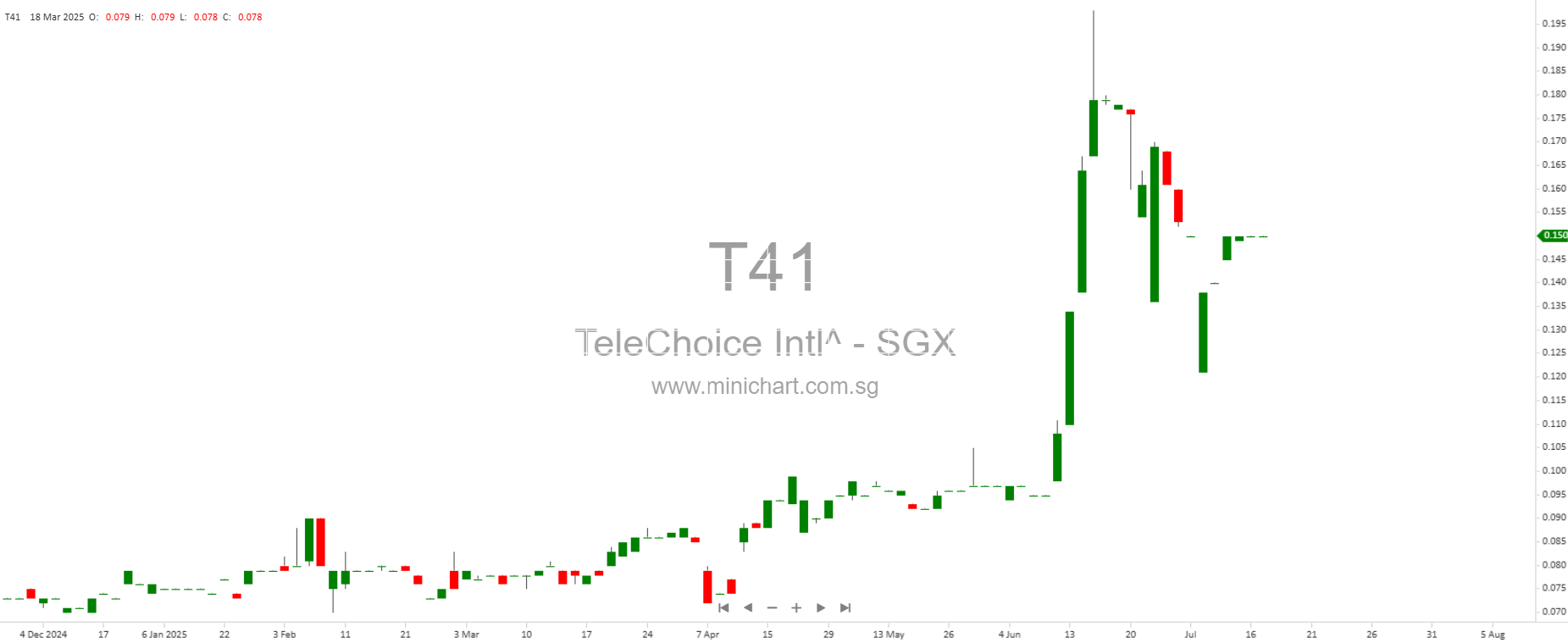

Share price performance has also reflected renewed investor confidence — climbing 87.5% year-to-date to 15 cents as of July 16.

Wong has formally requested that TeleChoice be removed from the SGX watchlist, noting that its $70 million market cap far exceeds the $40 million threshold.

“We are clearly rebuilding for sustainable and long-term growth,” she affirms.

Market Recognition and Outlook

In a March 4 unrated report, Maybank Securities analyst Hussaini Saifee acknowledged TeleChoice’s return to profitability and the dividend resumption of 0.125 cents per share. He noted that the company expects continued revenue growth across all segments, despite macroeconomic uncertainty.

Although the success of its five-year transformation plan (culminating in FY2029’s “year of great expectations”) remains to be seen, early signs are promising. PBT rose to $1.3 million in 1QFY2024, up from $200,000 in the same period the year before.

Shareholders have taken notice. One wrote: “TeleChoice’s profit is an encouraging step forward. Great job, thumbs up!”

Another echoed: “Thanks for the effort, the improvements this quarter are heading in the right direction. Keep it up!”

Thank you