Maybank Research Pte Ltd

April 25, 2025

Mapletree Logistics Trust: Navigating Trade Tensions with a Cautious Outlook

Mapletree Logistics Trust (MLT SP) faces headwinds from falling distributions and trade tensions, but its reasonable valuation merits a BUY rating.

Key Takeaways from MLT’s 4QFY24/25 Performance

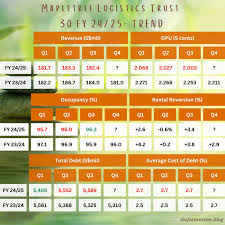

- MLT reported a 4QFY24/25 distribution per unit (DPU) of SGD1.955 cents, marking a decrease of 2.4% quarter-over-quarter and 11.6% year-over-year [[1]].

- The full-year DPU stood at SGD8.053 cents, a 10.6% decrease compared to the previous year [[1]].

- Higher borrowing costs, weakness in China, and reduced divestment gains impacted the distribution [[1]].

- Portfolio occupancy remained stable, and rental reversions were positive, excluding China [[1]].

- Gearing saw a slight increase, while debt cost and coverage ratios remained stable [[1]].

Financial Performance Analysis

MLT’s financial results reflect both resilience and challenges in the current economic climate [[1]].

- 4Q revenue was SGD179.6 million, down 1.5% QoQ and 0.8% YoY [[1]].

- Net property income (NPI) for 4Q was SGD152.8 million, a decrease of 2.8% QoQ and 1.6% YoY [[1]].

- Full-year revenue reached SGD727 million, and NPI was SGD625.3 million, representing declines of 0.9% and 1.5% YoY, respectively [[1]].

- Weakness in China, portfolio reconstitution, FX volatility, and lower margins influenced the results [[1]].

- Borrowing costs increased YoY due to repricing but decreased QoQ, benefiting from lower interest rates on unhedged loans [[1]].

The decline in DPU was primarily due to lower distribution of divestment gains [[1]]. Portfolio occupancy remained strong at 96.2% [[1]]. Gains in Japan and China offset declines in Singapore, Malaysia, and Vietnam [[1]]. Management indicated that 85% of group revenue comes from tenants serving domestic consumption, though export-oriented economies like Singapore and Vietnam experienced impacts from warehousing pulled-back orders [[1]]. Rent reversion was +5.1% (+6.9% ex-China) for 4Q, compared to +3.4% (+5.4% ex-China) for 3Q [[1]]. China’s reversion was less negative at -9.4% compared to -10.2% [[1]]. Focus remains on tenant retention due to substantial revenue from China due for renewal this FY [[1]].

Capital Management and Portfolio Valuation

MLT maintains a prudent approach to capital management [[1]].

- Gearing stood at 40.7% (up from 40.3% in 3Q), with a stable debt cost of 2.7% and a coverage ratio of 2.9x [[1]].

- Portfolio valuation remained stable due to capital expenditure and M&As, offset by FX translation losses and fair value losses in Singapore, Hong Kong, China, and South Korea due to higher cap rates [[2]].

- Macro uncertainties and regional trade evolution may influence the pace of capital recycling [[2]].

Revised Target Price and Recommendation

Despite a cautious outlook, Maybank retains a BUY recommendation [[2]].

- DPU estimate lowered by 3.7% for FY25/26 due to the absence of divestment gains [[2]].

- The DDM-based target price is trimmed to SGD1.30 from SGD1.35 [[2]].

- The BUY recommendation is maintained based on a reasonable valuation with a 6% yield and 0.9x PB [[2]].

Key Statistics

- Share Price: SGD 1.16 [[2]]

- 12m Price Target: SGD 1.30 (+16%) [[2]]

- Previous Price Target: SGD 1.35 [[2]]

- 52w high/low (SGD): 1.49/1.05 [[2]]

- 3m avg turnover (USDm): 74.2 [[2]]

- Free float (%): na [[2]]

- Issued shares (m): 4,994 [[2]]

- Market capitalisation: SGD5.8B/USD4.4B [[2]]

- Major shareholders: Temasek Holdings Pte Ltd. (Investment Co 25.8%) [[2]]

Financial Table

| FYE Mar (SGD m) | FY24A | FY25A | FY26E | FY27E | FY28E |

|---|---|---|---|---|---|

| Revenue | 734 | 727 | 718 | 729 | 740 |

| Net property income | 635 | 625 | 621 | 631 | 640 |

| Core net profit | 447 | 406 | 357 | 370 | 378 |

| Core EPU (cts) | 6.8 | 6.2 | 5.5 | 5.6 | 5.6 |

| Core EPU growth (%) | 0.4 | (8.0) | (12.3) | 2.4 | 1.0 |

| DPU (cts) | 9.0 | 8.1 | 7.0 | 7.1 | 7.2 |

| DPU growth (%) | (0.1) | (10.6) | (13.1) | 2.1 | 0.8 |

| P/NTA (x) | 1.1 | 1.0 | 0.9 | 0.9 | 0.9 |

| DPU yield (%) | 6.2 | 6.1 | 6.0 | 6.2 | 6.2 |

| ROAE (%) | 4.9 | 4.6 | 4.2 | 4.3 | 4.3 |

| ROAA (%) | 3.3 | 2.9 | 2.6 | 2.6 | 2.7 |

| Debt/Assets (x) | 0.38 | 0.40 | 0.40 | 0.40 | 0.39 |

| Consensus DPU | – | – | 8.0 | 8.0 | 7.7 |

| MIBG vs. Consensus (%) | – | – | (12.5) | (10.7) | (5.8) |

Risks to Consider

Several factors could impact MLT’s performance [[3]]:

- Slower growth in China

- Escalating trade tensions

- Slower pace of capital recycling

- Higher interest rates

- FX translation losses

Value Proposition

MLT is the second-largest industrial sector S-REIT, backed by sponsor Mapletree Investments (Temasek Holdings) [[4]]. Its portfolio has grown significantly since its IPO in 2005, diversifying across nine Asian geographies [[4]]. MLT focuses on capital recycling and redevelopment, aiming to enhance NAV growth [[4]].

Price Drivers and Historical Share Price Trends

Key events have influenced MLT’s share price [[4]]:

- Jan-20: Acquisition of Kobe Logistics Centre [[4]].

- Oct-20: Acquisition of nine assets in China, Malaysia, and Vietnam [[4]].

- Nov-21: Acquisition of warehouses in China, Vietnam, and Japan [[4]].

- Mar-23: Non-redemption of SGD180m perp, acquisition of warehouses in Japan, Sydney, and Korea [[4]].

- 2024: Acquisitions in Malaysia, India, and Vietnam, divestment of SGD237m, and change of CEO [[4]].

Financial Metrics and Swing Factors

Capital recycling, divestment gains, and currency appreciation support distribution [[4]]. NPI margins are expected to stabilize, with a well-staggered lease expiry profile [[4]]. Upside factors include improved leasing demand and rental reversion, while downside risks include economic slowdown, lease terminations, FX volatility, and rising interest rates [[4]].

ESG Assessment

MLT’s ESG profile reveals several key considerations [[5]]:

- Business Model & Industry Issues: Susceptible to sustainability-focused investors due to its need for additional capital. Regulated by MAS under Singapore’s code on collective investment schemes [[5]].

- Material E issues: Focus on energy intensity reduction and renewable energy. Secured SGD800m of green funding [[5]].

- Key G metrics and issues: Externally managed by a subsidiary of Mapletree Investments. Board comprises 12 directors, with 7 independent and 4 females [[5]].

- Material S issues: Aligned initiatives to sponsor’s CSR framework. High gender diversity [[5]].

Financial Statement Summary

Key figures from the financial statements [[6]]:

- Revenue: FY24A: 733.9, FY25A: 727.0, FY26E: 718.3, FY27E: 729.1, FY28E: 740.0

- Net Property Income: FY24A: 634.9, FY25A: 625.3, FY26E: 621.3, FY27E: 630.7, FY28E: 640.1

- Core Net Profit: FY24A: 447.1, FY25A: 406.4, FY26E: 357.1, FY27E: 369.6, FY28E: 377.9

- Distributable Income to Unitholders: FY24A: 447.1, FY25A: 406.4, FY26E: 357.1, FY27E: 369.6, FY28E: 377.9

Key Ratios Analysis

Key ratios provide insights into MLT’s performance and financial health [[7]]:

- Revenue Growth: FY24A: 0.4, FY25A: (0.9), FY26E: (1.2), FY27E: 1.5, FY28E: 1.5

- Net Property Income Growth: FY24A: 0.0, FY25A: (1.5), FY26E: (0.6), FY27E: 1.5, FY28E: 1.5

- Core Net Profit Growth: FY24A: 3.3, FY25A: (9.1), FY26E: (12.1), FY27E: 3.5, FY28E: 2.2

- Net Gearing (%): FY24A: 66.9, FY25A: 72.9, FY26E: 71.6, FY27E: 70.2, FY28E: 68.9